Contact our offices

Main office

COLBURN

5 & 6 BAILEY COURT

COLBURN BUSINESS PARK

RICHMOND

NORTH YORKSHIRE

DL9 4QL

Estate Agency Offices are located in

BOROUGHBRIDGE & RICHMOND

Residential Management Team

Our Offices

- Alnwick

01665 568310

Email Officealnwick@gscgrays.co.uk - Boroughbridge

01423 590500

Email Officeboroughbridge@gscgrays.co.uk - Chester-Le-Street

0191 3039540

Email Officechester-le-street@gscgrays.co.uk - Colburn

01748 897630

Email Officecolburn@gscgrays.co.uk - Driffield

01377 337180

Email Officedriffield@gscgrays.co.uk - Hamsterley

01388 487000

Email Officehamsterley@gscgrays.co.uk - Hexham

01434 611565

Email Officehexham@gscgrays.co.uk - Kirkby Lonsdale

01524 880320

Email Officekirkbylonsdale@gscgrays.co.uk - Penrith

01768 597005

Email Officepenrith@gscgrays.co.uk

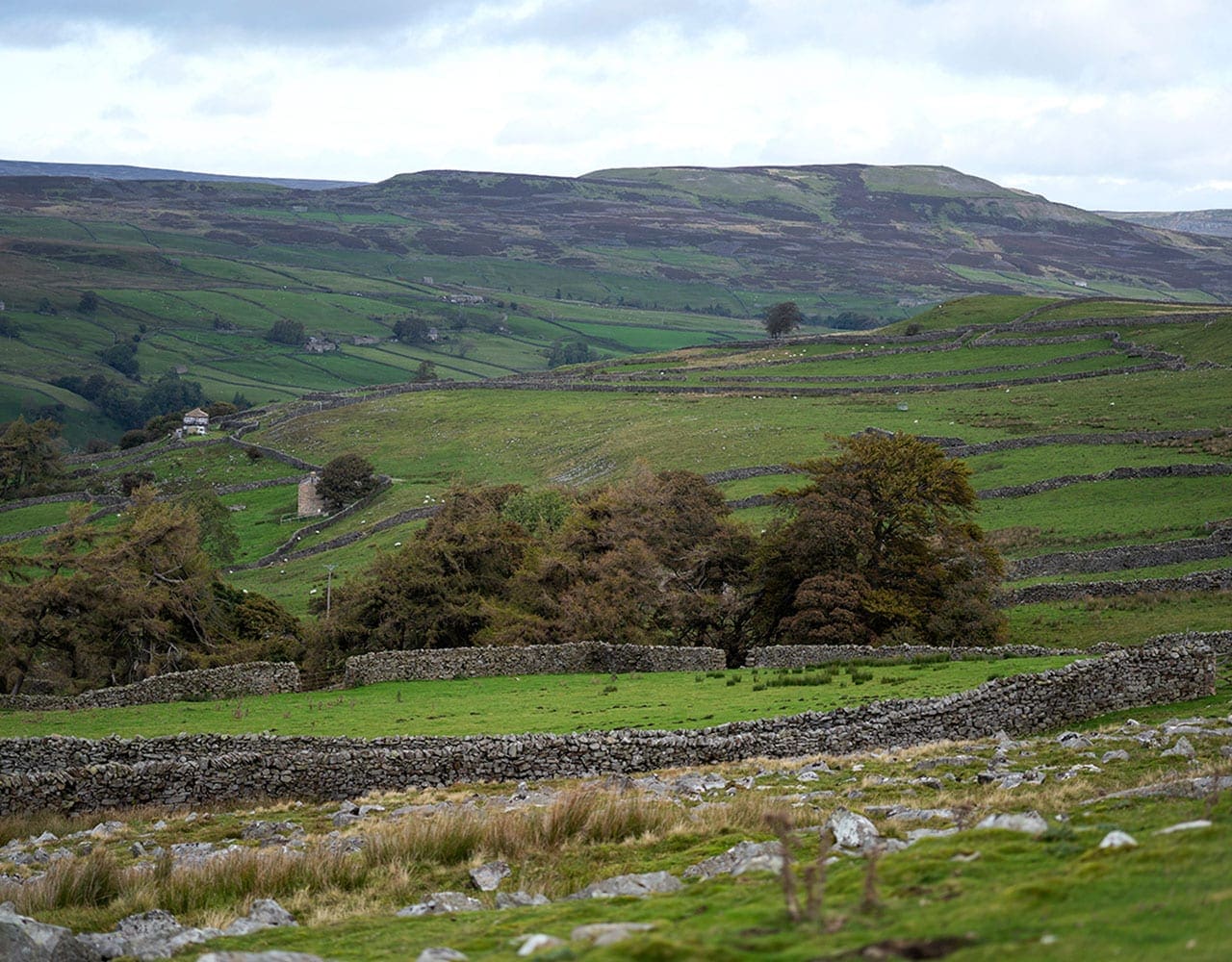

HOW THE MARKET HAS PERFORMED IN 2020: FARMS AND FARMLAND

Although there has been a late flurry in 2020, the farm market has been dominated by the impact of the fallout from COVID-19. This was the year that agents were predicting a return to more normal volumes of land being offered for sale having had two years of record low supplies, but it has not turned out that way. At the end of September, the national offering of land advertised had fallen by 40% year on year to less than 50,000 acres although in Yorkshire and the North East the reduction is only marginal, dominated in acreage terms by a single 1,142 acre farm in Northumberland near Cornhill-on-Tweed which now has a closing date for best bids at the end of October – the market will watch with interest the result of that. Furthermore, expectations were that with an increase in supply, land values would come under pressure as Brexit became a reality with the passing of the European Union (Withdrawal Agreement) Act 2020, and more became known about the replacement of farming subsidies and how they would impact on incomes. None of these market influences have come to pass as demand continues to outstrip the meager supply and prices, if anything, has increased a little on those of last year halting a three-year downward trend.

Continuing a trend of the last few years the range of prices achieved remains wide. Blocks of bare arable land have again achieved over £10,000+ per acre for the very best whilst more marginal land has struggled to reach £5,500 per acre nationally. In our region we have analysed the spread of land values, from successful bare land and whole farm sales at an average of between £6,690 and £8700 per acre but due to the number of smaller farms offered, particularly in highly sought after residential areas of North Yorkshire, overall farm prices have been encouragingly strong. As ever special purchasers have heavily influenced the market. Neighbours have bid strongly when the opportunity arises and non-farming buyers have been active for smaller units.

Rollover has played a part again this year, although not to quite the same extent as the previous three years. Sales are taking noticeably longer to transact, which is causing some frustration in the market. Under-staffed local authorities are taking between six and ten weeks to get searches back, whilst valuers, conveyancers and funders are struggling to cope with demand, due to high levels of residential sales.

As for the near future, we are certainly expecting things to settle down and our predictions for the coming year are similar to those of this year before COVID-19 took hold. Of our own clients, there are a range of differing views; some are keen to press ahead, having taken the view that prices will not get any better in the short term, whilst others are taking a more pragmatic approach, preferring to wait until some of the uncertainty is out of the market and more is known about Environmental Land

Management (ELM), the value of natural capital and seeing where they can add value before committing to sell. There is no right answer, but we can’t help thinking that land prices are only likely to come under further pressure as incomes are squeezed and while the cost of borrowed money remains as low as it is, now is the time to sell, if all other options have been exhausted.

Client Feedback

We have had the pleasure of serving a variety of clients...

We received excellent service and were well informed at each stage of the process. We were pleasantly surprised when Kate whooped down the phone when she received the key for Golden Lion Mews! We would have no hesitation in giving you and the team 5 stars for service.

Mr and Mrs Marron

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays provide an experienced and professional service. From the initial contact with the valuer (Graham Wood) to the closure of the sale they keep you informed throughout. Graham and all of the staff are a pleasure to deal with. I would highly recommend them. I would also give you a 5 star rating.

Marian Lowe

Client Feedback

We have had the pleasure of serving a variety of clients...

I unhesitatingly recommend Gray’s Estate Agent in Barnard Castle. We explored a number of agents and chose GSC Grays not because they were the cheapest but because they most inspired our confidence. We were not disappointed; from the initial visit through various stages to completion we were impressed by the professionalism, attention to detail, excellent communication, competent negotiation, and willingness to go the extra mile in customer service. They facilitated the sale of our property in a way that made it feel a pleasure to sell.

H. Thorp

Client Feedback

We have had the pleasure of serving a variety of clients...

We have moved house several times over the years so feel well qualified to recognise good efficient service when we see it. All the way through, from the initial valuation to the day of completion, everyone at GSC Grays made us feel our sale really mattered. We were kept well informed of the progress of the sale and any questions we had were answered promptly and clearly. We would definitely recommend GSC Grays to anyone planning to buy or sell a property.

M. Scarborough

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you once again for the excellent care you have taken of us during the sale and now the purchase of our house. We have felt all along that you really cared and were really interested. A wonderful service.

A. Merck

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you for all your help during our move. It all got quite stressful towards the end and it was great to have you at the end of the phone offering reassurance and advice. We got there in the end and we are delighted with our new home! Just wanted to let you know how much your help was appreciated!

Katy

Client Feedback

We have had the pleasure of serving a variety of clients...

I just wanted to pass on my appreciation to the whole team for the fantastic job they did for me. The Sales Progression team had a particularly tricky job as the sale was less than easy but they were all amazing.

G.F

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays were recommended to me and in the years which I have worked with them, I have found their approach excellent. They take a long term view and provide exactly the right balance between pushing things on whilst keeping me informed – I am delighted to have them on board.

C.C

Client Feedback

We have had the pleasure of serving a variety of clients...

Excellent HomeBuyer Report service. Survey completed promptly and initial comments delivered by telephone within twenty-four hours with comprehensive written report received by post shortly after. Clear, concise documentation, which includes advice on rectifying defects and issues that legal advisors may wish to investigate, all professionally presented in a bound booklet enabling a timely informed decision to be achieved in respect of the purchase of the property. Thoroughly recommended.

A. Longstaff

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays have always provided a professional and friendly letting service for me. Their regular updates and communication have meant total peace of mind that my properties are being managed with the up most of care. I would definitely recommend GSC Grays to other landlords.

M.M

Client Feedback

We have had the pleasure of serving a variety of clients...

When your largest cost in selling/purchasing a new house is the estate agent fees it is a rather large cost to accept, especially with things like Rightmove been involved. However, once my sale was agreed and it was passed over to Catherine in the sales progression team I do believe the fee was easier to stomach as her role in the sale/purchase was worth its weight in gold, and without it, there is no doubt in my mind that things would have not got done in the timescales we and our seller wanted. I really do appreciate all of Catherine’s advice and help in keeping the whole process moving.

E. Sword

Lycetts

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you so much to the Barnard Castle Branch and the Sales Progression team for all your help with the purchase of our new home. We are absolutely delighted with the property and were really impressed by the service and experience we had at GSC Grays.

H. Langford

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you to everyone at GSC Grays for your friendly professionalism over the past two years and especially in more recent weeks. I greatly appreciated all you do and would have no hesitation in recommending you to anyone!

J.N

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays were recommended to me and in the years in which I have worked with them, I have found their approach excellent. They take a long term view and provide exactly the right balance between pushing things on whilst keeping me informed – I am delighted to have them on board.

A.N

Client Feedback

We have had the pleasure of serving a variety of clients...

Theakston Land has worked with Calum and his team for many years. That work has included a detailed analysis of costs to maximise value. The development appraisal work undertaken with GCS Grays means that I am confident we are getting the best possible price. They make a positive contribution at all levels and help to drive forward long term and complex development projects.

S Marlow

Theakston Land

Client Feedback

We have had the pleasure of serving a variety of clients...

During 2020 Holly Story has worked on Barningham Estate helping us in our understanding of Natural Capital assets. Holly was instrumental in Barningham’s successful ELMs Test and Trial bid and is leading in the bid’s implementation. Her understanding and thought leadership are helping to bring clarity and good sense to what seems an increasingly complicated agricultural world.

Sir Edward Milbank

Barningham Estate

Client Feedback

We have had the pleasure of serving a variety of clients...

We have been working with GSC Grays Farm Business team since 2018 and with Robert Sullivan for over 20 years. The advice and insight of the team has been invaluable and means that we are now in a much stronger position to face the future and the changes in the industry with confidence. Their passion and commitment to us and the farm is integral to our success.

T. Dent

Dinsdale Farming Ltd.

Client Feedback

We have had the pleasure of serving a variety of clients...

We could not have chosen a better estate agent. Excellent work from start to finish from all the well-motivated professionals with whom we came into contact. The house was well marketed, and communications were superb, we were always kept well informed.

Mrs A

© COPYRIGHT GSC GRAYS LIMITED

TRADING AS GSC GRAYS (ENGLAND AND WALES). COMPANY REGISTRATION NUMBER: 07715034.

REGISTERED OFFICE ADDRESS:

1 BAILEY COURT, COLBURN BUSINESS PARK, RICHMOND, NORTH YORKSHIRE DL9 4QL

Contact our offices

Main office

COLBURN

5 & 6 BAILEY COURT

COLBURN BUSINESS PARK

RICHMOND

NORTH YORKSHIRE

DL9 4QL

Estate Agency Offices are located in...

BOROUGHBRIDGE & RICHMOND

Residential Management Team

Our Offices

- Alnwick

01665 568310

alnwick@gscgrays.co.uk - Boroughbridge

01423 590500

boroughbridge@gscgrays.co.uk - Chester-Le-Street

0191 3039540

chester-le-street@gscgrays.co.uk - Colburn

01748 897630

colburn@gscgrays.co.uk - Driffield

01377 337180

driffield@gscgrays.co.uk - Hamsterley

01388 487000

hamsterley@gscgrays.co.uk - Hexham

01434 611565

hexham@gscgrays.co.uk - Kirkby Lonsdale

01524 880320

kirkbylonsdale@gscgrays.co.uk - Penrith

01768 597005

penrith@gscgrays.co.uk

Or please fill in your details below and one of our team will get back to you as soon as possible.