Contact our offices

Main office

COLBURN

5 & 6 BAILEY COURT

COLBURN BUSINESS PARK

RICHMOND

NORTH YORKSHIRE

DL9 4QL

Estate Agency Offices are located in

BARNARD CASTLE, BOROUGHBRIDGE & RICHMOND

Residential Management Team

Our Offices

- Alnwick

01665 568310

Email Officealnwick@gscgrays.co.uk - Barnard Castle

01833 637000

Email Officebarnardcastle@gscgrays.co.uk - Boroughbridge

01423 590500

Email Officeboroughbridge@gscgrays.co.uk - Chester-Le-Street

0191 3039540

Email Officechester-le-street@gscgrays.co.uk - Colburn

01748 897630

Email Officecolburn@gscgrays.co.uk - Driffield

01377 337180

Email Officedriffield@gscgrays.co.uk - Hamsterley

01388 487000

Email Officehamsterley@gscgrays.co.uk - Hexham

01434 611565

Email Officehexham@gscgrays.co.uk - Kirkby Lonsdale

01524 880320

Email Officekirkbylonsdale@gscgrays.co.uk - Penrith

01768 597005

Email Officepenrith@gscgrays.co.uk

THE FARMLAND MARKET-AUTUMN 2021

Supply to the UK farmland market has increased year on year with around 55,000 acres being offered for sale on the open market according to the Farmers Weekly annual tally to the end of September.

Whilst there has been an 11% annual increase in land brought to the market, only 1,234 acres of land was brought to the market at the end of September, representing a -23% difference compared to this time last year.

Demand for this land has been steady, driven, in the main by farmer buyers but also by lifestyle and institutional buyers with a keen eye on environment and sustainability opportunities.

In our region of North Yorkshire, County Durham, Northumberland and Cumbria, we have a similar message to report with supply levels up across the market sector with noticeably more arable acres (although mainly in bare land parcels) than in recent years.

Farmers have been more active than non-farmers than in recent years with rollover funds released from the increasing demand for house building land, driving prices through competitive bidding, particularly on prime arable land.

Competition is also increasing from several sectors on more marginal and hill land driven by demand for tree planting and other environment and sustainability criteria.

Whilst discussions around possible retirement have become more regular, encouraged by the ‘lump sum exit scheme’, ultimately decisions on whether to leave the industry have come down to timing rather than any meaningful retirement incentive. Selling while demand is high and bidding competitive, has been much more likely to achieve a larger retirement pot, further supported by a favourable capital tax regime.

Much less has been said about the impact caused by lifestyle buyers moving to the countryside in the search for more space. Such demand impacts on smaller land parcel sales and can distort average farmland price figures if not carefully analysed. Even with CGT to pay, small parcel sales can be hugely profitable for farmers selling to these buyers, but it makes it overly expensive for those wishing to add to their existing farm holdings.

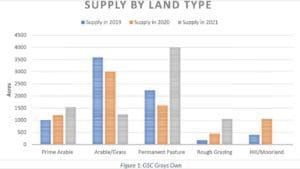

In summary, arable, rotational grass and most permanent pasture has seen values measured in low single figure increases this year as supply has generally been met by demand. Average prime arable land in North Yorkshire and the North East levels out at approximately £10,800 while rotational grassland is averaging £8,000 per acre as shown in the graph above taken from our own data sourcing.

Grassland farms in Cumbria and West Northumberland are averaging at approximately £6,500 per acre.

The most dramatic changes have been on rough and hill ground with some extraordinary bidding experienced in the hills of the Dales and the North Pennines. The main driver is forestry planting land with bidding from private individuals, consortiums, ESG motivated funds and institutions battling it out for a limited number of plantable acres.

Prices of £4,000 per acre are being offered without planning consent for afforestation. This translates through to equally exceptional prices being achieved for mature forests with timber prices at their highest level for many years, and supply in our region very limited. Buyers are generally heading for Scotland for greater opportunity with prices for the best mature woods exceeding £12,000 per acre (£30,000 per hectare).

Forecasting next year’s market trends is increasingly difficult with new market influences entering the arena. We remain unclear how much natural capital will influence land values, nor the level of demand from big business or institutional investors with ESG their motivating interest. BPS payments will be further reduced, but hopefully the value of support through Environmental Land Management (ELM) will become clearer but there is no doubt that the focus will move the market further away from food production and closer to creating greater natural capital.

We have been expecting for some time now, changes to be made to the treatment of capital taxation on our farms and land sales. The removal of Agricultural Property Relief is all but inevitable and if it is not announced in the October Financial Review it will surely be delivered in the Spring 2022 Budget. This will impact most on those who have bought farms to shelter wealth from Inheritance Tax, usually non-farming buyers and this may well curb demand and impact competition in the market.

There is still some way to go before the impact of all these changes will be felt in the land market and we therefore predict that the old influences of supply and demand will be the simple drivers of the direction of land prices next year. Increases of between 3% and 5% are expected on average although if the clamour to buy land for tree planting continues to grow, significantly greater increases could be seen on suitable planting land.

GSC Grays News

Prospects for UK Land Demand: Why Rural Assets Remain an Investment Safe Haven

Read more

Client Feedback

We have had the pleasure of serving a variety of clients...

We received excellent service and were well informed at each stage of the process. We were pleasantly surprised when Kate whooped down the phone when she received the key for Golden Lion Mews! We would have no hesitation in giving you and the team 5 stars for service.

Mr and Mrs Marron

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays provide an experienced and professional service. From the initial contact with the valuer (Graham Wood) to the closure of the sale they keep you informed throughout. Graham and all of the staff are a pleasure to deal with. I would highly recommend them. I would also give you a 5 star rating.

Marian Lowe

Client Feedback

We have had the pleasure of serving a variety of clients...

I unhesitatingly recommend Gray’s Estate Agent in Barnard Castle. We explored a number of agents and chose GSC Grays not because they were the cheapest but because they most inspired our confidence. We were not disappointed; from the initial visit through various stages to completion we were impressed by the professionalism, attention to detail, excellent communication, competent negotiation, and willingness to go the extra mile in customer service. They facilitated the sale of our property in a way that made it feel a pleasure to sell.

H. Thorp

Client Feedback

We have had the pleasure of serving a variety of clients...

We have moved house several times over the years so feel well qualified to recognise good efficient service when we see it. All the way through, from the initial valuation to the day of completion, everyone at GSC Grays made us feel our sale really mattered. We were kept well informed of the progress of the sale and any questions we had were answered promptly and clearly. We would definitely recommend GSC Grays to anyone planning to buy or sell a property.

M. Scarborough

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you once again for the excellent care you have taken of us during the sale and now the purchase of our house. We have felt all along that you really cared and were really interested. A wonderful service.

A. Merck

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you for all your help during our move. It all got quite stressful towards the end and it was great to have you at the end of the phone offering reassurance and advice. We got there in the end and we are delighted with our new home! Just wanted to let you know how much your help was appreciated!

Katy

Client Feedback

We have had the pleasure of serving a variety of clients...

I just wanted to pass on my appreciation to the whole team for the fantastic job they did for me. The Sales Progression team had a particularly tricky job as the sale was less than easy but they were all amazing.

G.F

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays were recommended to me and in the years which I have worked with them, I have found their approach excellent. They take a long term view and provide exactly the right balance between pushing things on whilst keeping me informed – I am delighted to have them on board.

C.C

Client Feedback

We have had the pleasure of serving a variety of clients...

Excellent HomeBuyer Report service. Survey completed promptly and initial comments delivered by telephone within twenty-four hours with comprehensive written report received by post shortly after. Clear, concise documentation, which includes advice on rectifying defects and issues that legal advisors may wish to investigate, all professionally presented in a bound booklet enabling a timely informed decision to be achieved in respect of the purchase of the property. Thoroughly recommended.

A. Longstaff

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays have always provided a professional and friendly letting service for me. Their regular updates and communication have meant total peace of mind that my properties are being managed with the up most of care. I would definitely recommend GSC Grays to other landlords.

M.M

Client Feedback

We have had the pleasure of serving a variety of clients...

When your largest cost in selling/purchasing a new house is the estate agent fees it is a rather large cost to accept, especially with things like Rightmove been involved. However, once my sale was agreed and it was passed over to Catherine in the sales progression team I do believe the fee was easier to stomach as her role in the sale/purchase was worth its weight in gold, and without it, there is no doubt in my mind that things would have not got done in the timescales we and our seller wanted. I really do appreciate all of Catherine’s advice and help in keeping the whole process moving.

E. Sword

Lycetts

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you so much to the Barnard Castle Branch and the Sales Progression team for all your help with the purchase of our new home. We are absolutely delighted with the property and were really impressed by the service and experience we had at GSC Grays.

H. Langford

Client Feedback

We have had the pleasure of serving a variety of clients...

Thank you to everyone at GSC Grays for your friendly professionalism over the past two years and especially in more recent weeks. I greatly appreciated all you do and would have no hesitation in recommending you to anyone!

J.N

Client Feedback

We have had the pleasure of serving a variety of clients...

GSC Grays were recommended to me and in the years in which I have worked with them, I have found their approach excellent. They take a long term view and provide exactly the right balance between pushing things on whilst keeping me informed – I am delighted to have them on board.

A.N

Client Feedback

We have had the pleasure of serving a variety of clients...

Theakston Land has worked with Calum and his team for many years. That work has included a detailed analysis of costs to maximise value. The development appraisal work undertaken with GCS Grays means that I am confident we are getting the best possible price. They make a positive contribution at all levels and help to drive forward long term and complex development projects.

S Marlow

Theakston Land

Client Feedback

We have had the pleasure of serving a variety of clients...

During 2020 Holly Story has worked on Barningham Estate helping us in our understanding of Natural Capital assets. Holly was instrumental in Barningham’s successful ELMs Test and Trial bid and is leading in the bid’s implementation. Her understanding and thought leadership are helping to bring clarity and good sense to what seems an increasingly complicated agricultural world.

Sir Edward Milbank

Barningham Estate

Client Feedback

We have had the pleasure of serving a variety of clients...

We have been working with GSC Grays Farm Business team since 2018 and with Robert Sullivan for over 20 years. The advice and insight of the team has been invaluable and means that we are now in a much stronger position to face the future and the changes in the industry with confidence. Their passion and commitment to us and the farm is integral to our success.

T. Dent

Dinsdale Farming Ltd.

Client Feedback

We have had the pleasure of serving a variety of clients...

We could not have chosen a better estate agent. Excellent work from start to finish from all the well-motivated professionals with whom we came into contact. The house was well marketed, and communications were superb, we were always kept well informed.

Mrs A

Keep up to date

Register for our newsletters to receive the latest information on our services, the industry, and our own company news.

Subscribe to our newsletter© COPYRIGHT GSC GRAYS LIMITED

TRADING AS GSC GRAYS (ENGLAND AND WALES). COMPANY REGISTRATION NUMBER: 07715034.

REGISTERED OFFICE ADDRESS:

1 BAILEY COURT, COLBURN BUSINESS PARK, RICHMOND, NORTH YORKSHIRE DL9 4QL

Contact our offices

Main office

COLBURN

5 & 6 BAILEY COURT

COLBURN BUSINESS PARK

RICHMOND

NORTH YORKSHIRE

DL9 4QL

Estate Agency Offices are located in...

BARNARD CASTLE, BOROUGHBRIDGE & RICHMOND

Residential Management Team

Our Offices

- Alnwick

01665 568310

alnwick@gscgrays.co.uk - Barnard Castle

01833 637000

barnardcastle@gscgrays.co.uk - Boroughbridge

01423 590500

boroughbridge@gscgrays.co.uk - Chester-Le-Street

0191 3039540

chester-le-street@gscgrays.co.uk - Colburn

01748 897630

colburn@gscgrays.co.uk - Driffield

01377 337180

driffield@gscgrays.co.uk - Hamsterley

01388 487000

hamsterley@gscgrays.co.uk - Hexham

01434 611565

hexham@gscgrays.co.uk - Kirkby Lonsdale

01524 880320

kirkbylonsdale@gscgrays.co.uk - Penrith

01768 597005

penrith@gscgrays.co.uk

Or please fill in your details below and one of our team will get back to you as soon as possible.